One of the more vocal arguments against value investing stems from a belief that we’re in a “new normal” environment where innovative or high-tech companies have a leg up on “old guard” industries, such as energy or financials. FAANG stocks have typically been the poster children for this position; these behemoth technology companies have contributed meaningfully to the market’s overall return and, by virtue of being growth stocks, the negative value premiums in recent years. Well, guess who showed up as value this summer! That’s right, Russell reclassified Meta (formerly Facebook, the “F” in FAANG) and Netflix (the “N”) from growth to value during the index provider’s annual reconstitution event. Although signs have been pointing to the waning dominance of FAANG stocks since the start of 2022, it is somewhat ironic that 40% of the pillars supporting an aversion to value investing have now become value stocks themselves.

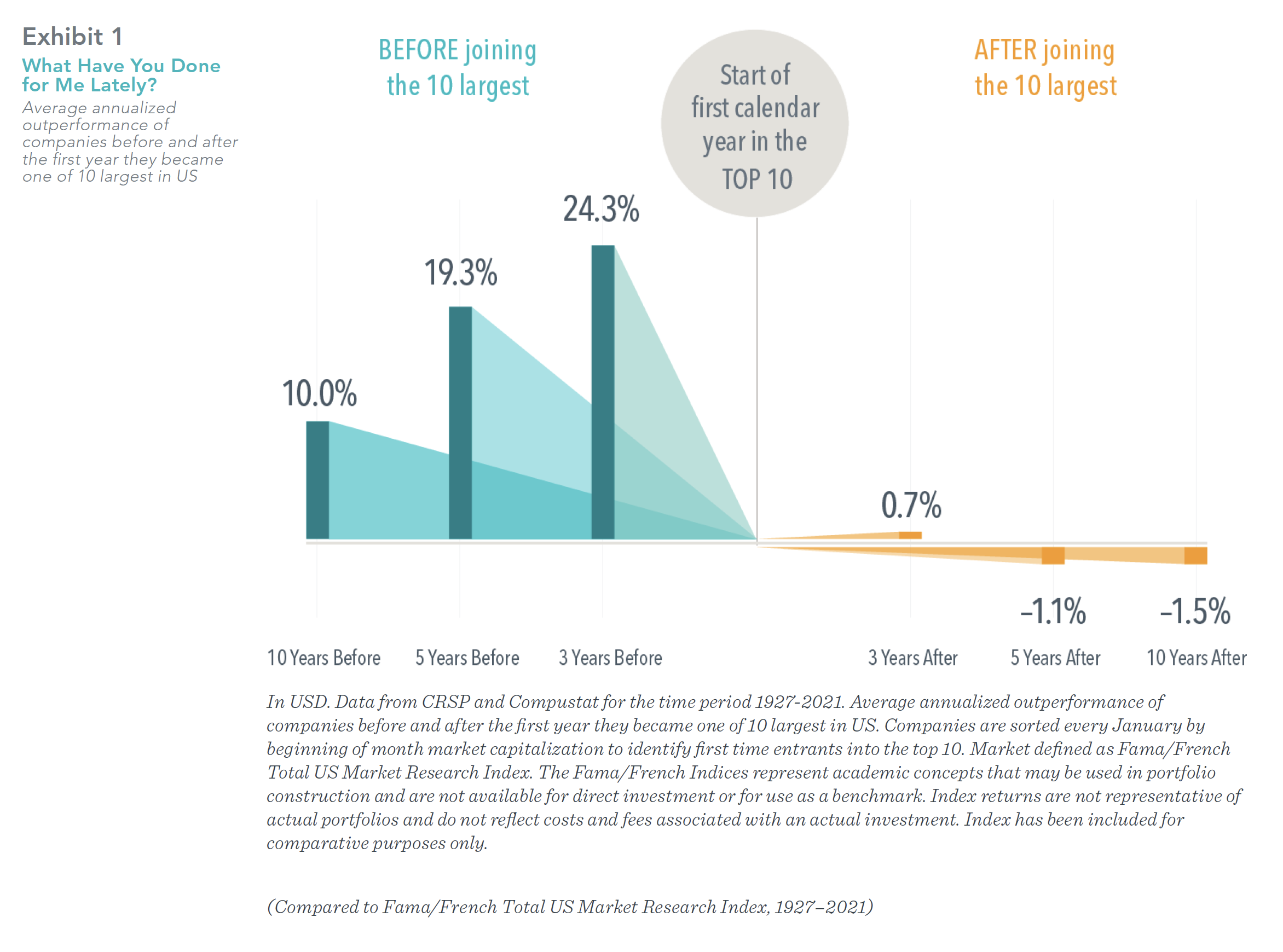

This also serves to highlight a possible misconception about the spirit of value investing. A value premium is a discount-rate effect: If expected future cash flows are not identically discounted for all stocks, then the ones with low prices relative to their expected future cash flows have higher expected returns. Investors advocating for the superiority of growth firms, such as the FAANGs, are inadvertently making the case for their expected future cash flows to be discounted at a lower level—all else equal, greater certainty around future success should be associated with a lower expected return. In fact, as Exhibit 1 shows, this is generally what we see for stocks of companies once they grow to become among the largest in the market. In other words, investors should be careful about equating expected company success with expected stock returns.

Past performance is no guarantee of future results.

DIMENSIONAL FUND ADVISORS AND TRIAD ADVISORS ARE NOT AFFILIATED.

The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. It is the responsibility of any persons wishing to make a purchase to inform

themselves of and observe all applicable laws and regulations. Unauthorized copying, reproducing, duplicating, or transmitting of this document are strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd, Dimensional Japan Ltd., and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

Share this article:

Investor Risk Capacity Survey

Receive Your Risk Number

Take a 5-minute survey that covers topics such as portfolio size, top financial goals, and what you’re willing to risk for potential gains. We’ll use your responses to pinpoint your exact Risk Number to guide our decision-making process.