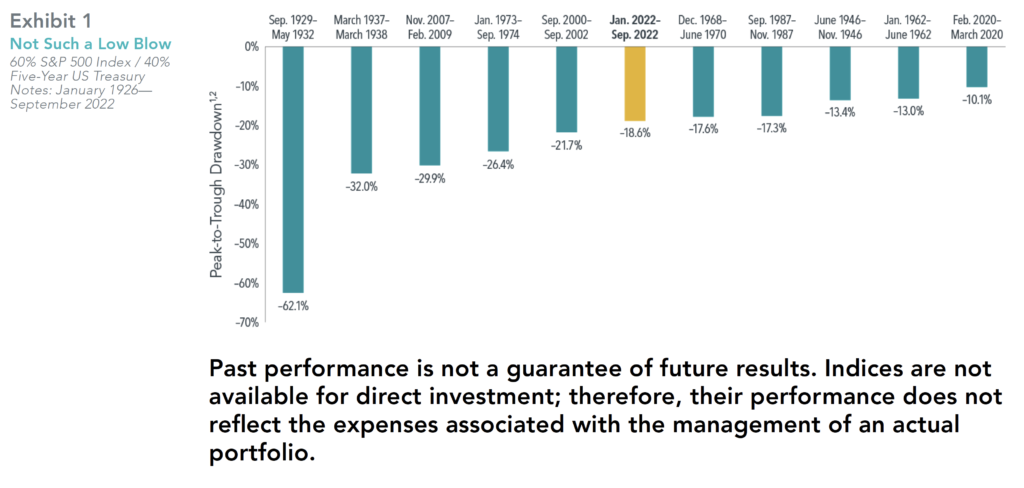

This has been a challenging year for investors. On top of the equity bear market, the steep losses in bonds1 have been especially surprising, leading some investors to question whether the classic 60/40 portfolio is dead. Although 2022 has seen the worst start to a year in history for many bond indices,1 the year-to-date experience for a 60/40 portfolio has not even cracked the top (or, alternatively, worst) five historical drawdowns of the last century. A 19% loss of wealth is not all that fun, but it’s only two-thirds of the drawdown investors endured through the financial crisis of 2008–2009 (see Exhibit 1).

A CASE FOR OPTIMISM

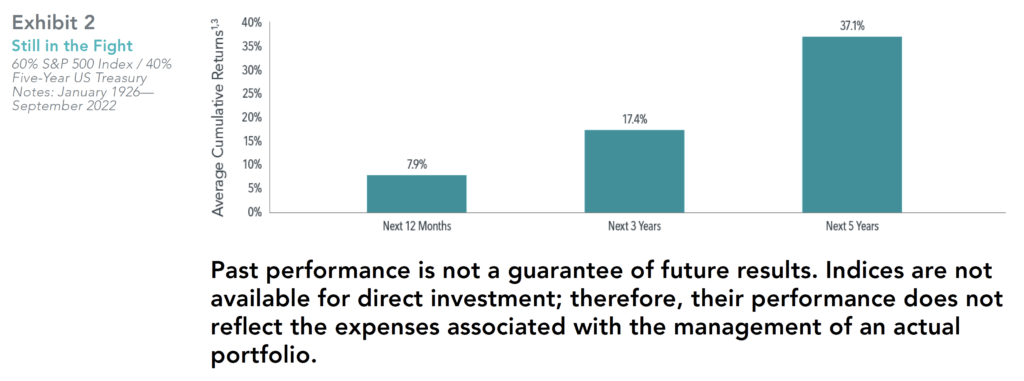

It is important, and especially so during difficult market conditions, for investors to focus not solely on where returns have been but also on where they could be going in the months and years ahead. Looking at the performance of a 60/40 portfolio following a decline of 10% or more since 1926 (see Exhibit 2), we see clearly that returns on average have been strong in the subsequent one-, three-, and five-year periods. History makes a strong case for investors to stick with their longer-term plan and should help serve as a reminder that steep declines shouldn’t derail investors’ progress toward reaping the expected benefits of investing.

ROLL WITH THE PUNCHES

Markets have proven quite resilient over the long run. Like a boxer stepping inside the ring, investors should expect (and prepare) to take a few shots and get pushed up against the ropes every so often. The most important thing, though, is to roll with the punches and not get knocked out by short-term moves. If history is any guide, there’s reason to believe the classic 60/40 portfolio is alive and well and could be poised to deliver healthy returns going forward.

1. Source: Morningstar Direct as of September 30, 2022.

2. In USD. The 60/40 portfolio consists of the S&P 500 Index (60%) and five-year US Treasury notes (40%). Rebalanced monthly. Peak-totrough drawdowns include all periods where the 60/40 portfolio declined by 10% or more from the prior peak. Peaks are defined as months where the 60/40 portfolio’s cumulative return exceeds all prior monthly observations. Troughs are defined as the months where the 60/40 portfolio’s cumulative return losses from the prior peak are the largest. Five-year US Treasury notes data provided by Morningstar. S&P data © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

3. In USD. The 60/40 portfolio consists of the S&P 500 Index (60%) and five-year US Treasury notes (40%). Rebalanced monthly. Drawdowns include all periods where the 60/40 portfolio declined by 10% or more from the prior peak. Peaks are defined as months where the 60/40 portfolio’s cumulative return exceeds all prior monthly observations. Returns are calculated for the one-, three-, and five-year look-ahead periods beginning the month after the 10% decline threshold is exceeded. The bar chart shows the average cumulative returns for the one-, three-, and five-year periods post decline. There are 10, nine, and nine observations for the one-, three-, and five-year look-ahead periods, respectively. Five-year US Treasury notes data provided by Morningstar. S&P data © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. It is the responsibility of any persons wishing to make a purchase to inform

themselves of and observe all applicable laws and regulations. Unauthorized copying, reproducing, duplicating, or transmitting of this document are strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd, Dimensional Japan Ltd., and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

Share this article:

Investor Risk Capacity Survey

Receive Your Risk Number

Take a 5-minute survey that covers topics such as portfolio size, top financial goals, and what you’re willing to risk for potential gains. We’ll use your responses to pinpoint your exact Risk Number to guide our decision-making process.