KEY TAKEAWAYS

- US stocks extended a bull market, with the S&P 500 reaching a series of record highs in the year’s first half, led by technology stocks.

- Core inflation fell slightly but remained above 3% in the US; the Fed kept rates steady, while central banks in Europe and Canada cut interest rates.

- Small cap and value stocks lagged the market, while high-profitability stocks outperformed, a reminder of the benefits of pursuing multiple premiums.

The beginning of 2024 started out a lot like the end of 2023, with markets rising amid talk of a potential decrease in US inflation and interest rate cuts from the Federal Reserve that could follow. But much like last year, those expectations remained unfulfilled, as core inflation fell slightly but held above 3% and the Fed stood pat on interest rates.1 US stocks as measured by the S&P 500 rose to a series of record highs in the year’s first half, and the benchmark 10-year US Treasury bond yield approached 5% in the spring before retreating.2

The Fed held a key measure, the federal funds rate, steady through June at 5.25%, the highest level in more than two decades, with officials citing an effort to cool persistently high inflation.3 Meanwhile, the European Central Bank cut rates for the first time since 2019, as did the Bank of Canada.4 US core inflation was 3.4% in May, a multiyear low but still well above the Fed’s 2% target. However, it has moved in the direction policymakers have said they’d like to see it go—lower—though they indicated at their meeting in June that they expect just one rate cut before the end of the year.5

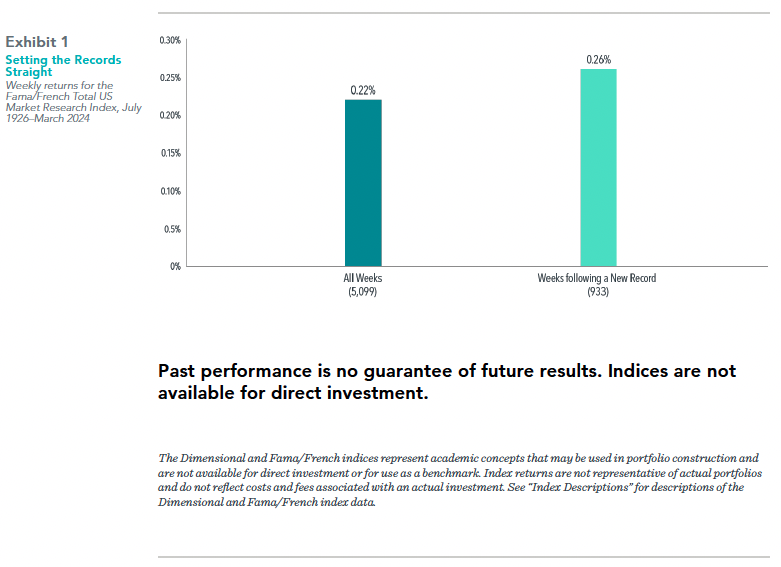

Against this backdrop, US stocks extended a bull market that began in late 2022, with the S&P 500 index gaining 14.6% through June 14 and notching new all-time highs. Record levels may lead some investors to wonder whether it’s a good time to sell, but historical data can help allay such concerns. Periodic record setting should be expected for an asset class with positive expected returns. As Exhibit 1 shows, the average return for weeks following these new highs was 0.26%—very close to the average return of 0.22% across all weeks. As long as investors demand positive returns in exchange for holding stocks, a new market high doesn’t mean the market is going to tumble.

The strong rally in the technology sector in 2023 continued into the new year. The techheavy Nasdaq, after gaining 44.6% last year, has risen 18.1% this year, vs. the S&P 500’s 14.6% gain. Nvidia remained the biggest driver of gains in the tech sector through the end of May, as demand remained strong for chips used to power cutting-edge AI applications.6 But expecting Nvidia and the rest of the so-called Magnificent 7 tech stocks to outperform the broader market is to bet on them further exceeding the market’s expectations.7 Simply meeting expectations may result in returns more in line with the market, consistent with the history of top US stocks.

Global stock markets reached multiyear highs, with the MSCI All Country World Index rising 10.6% through mid-June.8 Developed international stocks, as represented by the MSCI World ex USA Index, added 4.4%, and emerging markets stocks, as represented by the MSCI Emerging Markets Index, were up 6.4%.

US Treasuries were little changed for the year, with the 10-year Treasury bond falling 1.0%. However, yields (which rise when prices fall) remained higher than they have been for most of the past decade. The 10-year Treasury yield touched 4.7% in April, after nearly reaching 5% last October for the first time since 2007, before pulling back to 4.2% as of June 14.9

PUTTING PREMIUMS IN PERSPECTIVE

As the broader market gained, value stocks and the stocks of companies with small market capitalizations were unable to keep up with their historical outperformance. The MSCI All Country World Value Index rose 5.3%, about a third of the 15.7% increase for the MSCI All Country World Growth Index. Without help from the US tech sector, the MSCI All Country World ex USA Growth Index only rose 6.4%, still ahead of the 3.5% increase for the MSCI All Country World ex USA Value Index. Small cap companies underperformed large cap stocks globally: The MSCI All Country World Small Cap Index returned 1.3% vs. 10.6% for the larger-cap MSCI All Country World Index. But history suggests giving up on small cap value after prolonged stretches of underperformance in the past would have been a mistake.

And premiums don’t always move in lockstep, as stocks of companies with high profitability have recently outperformed the stocks of companies with low profitability. That has held true in both developed and emerging markets this year. The Fama/French Developed High Profitability Index rose 10.7% as of May 31, vs. 6.8% for its lowprofitability counterpart. The Fama/French Emerging Markets High Profitability Index rose 5.4%, while its low-profitability counterpart rose 0.7% as of May 31. It’s a reminder that investors who pursue multiple premiums can increase their chances of long-term success.10

THE BENEFITS OF A FLEXIBLE APPROACH

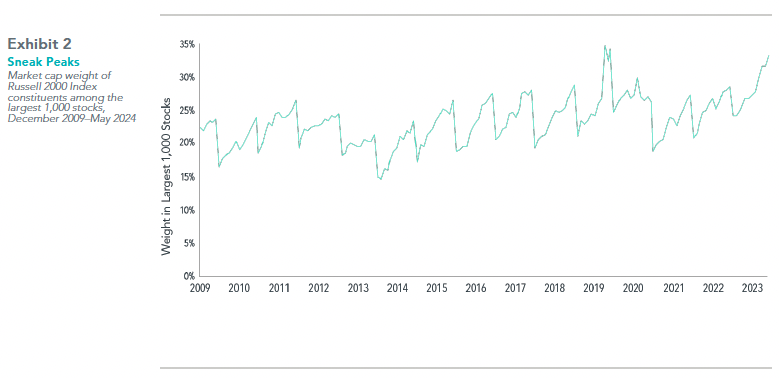

Pursuing historical premiums is one way of seeking to outperform benchmark returns. Implementation—including portfolio design, daily management, and trading—is another. Every June, an event helps put this into focus. That’s when Russell US indices undergo their “reconstitution,” when the benchmarks add and drop stocks. As time goes by, however, stock prices will change; what was once a small cap might become a large cap. Revising holdings annually means those stocks are stuck in the index, regardless of their characteristics, until the following June.

As Exhibit 2 shows, from December 2009 to May 2024, the small cap Russell 2000 Index had unsteady exposure to small caps. The percentage made up of large caps tended to rise through the year and peak before the index was reconstituted. That exposure to large caps came at the expense of a more consistent focus on small caps. In other words, investors may not have been getting what they came for. An investment process with the flexibility to evaluate and adjust holdings daily can provide a more consistent focus over time, potentially capturing premiums more reliably.

Investors who diversify, focus on the premiums, and embrace a flexible investing approach will still confront uncertainties in the year’s second half. But uncertainty is unavoidable, and it accounts for the risk that can lead to positive returns. How long can the bull market endure, and which way will inflation, and interest rates, go? Will the surge for AI-associated companies continue? Will global hostilities in the Middle East and Ukraine ease or increase? Will the US election bring a big November stock swing? (Spoiler: It usually hasn’t.) We’ll find out eventually, by the time the answers are also incorporated in market prices. Until then, 2024—like every year—is a good one for having a long-term plan and sticking with it.

DIMENSIONAL FUND ADVISORS AND TRIAD ADVISORS ARE NOT AFFILIATED.

The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. It is the responsibility of any persons wishing to make a purchase to inform

themselves of and observe all applicable laws and regulations. Unauthorized copying, reproducing, duplicating, or transmitting of this document are strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd, Dimensional Japan Ltd., and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

Share this article:

Investor Risk Capacity Survey

Receive Your Risk Number

Take a 5-minute survey that covers topics such as portfolio size, top financial goals, and what you’re willing to risk for potential gains. We’ll use your responses to pinpoint your exact Risk Number to guide our decision-making process.